Over the last decade, the agriculture sector has been contributing 25% of the national gross domestic product (GDP), while the share of agricultural workers in the total workforce stands at 66.4%. The Finscope 2020 Agriculture Finance Thematic Report – a deep dive analysis of the main Finscope 2020 Survey- shows that about 79% of the adult population is engaged in agriculture with 90% of farmers practicing subsistence farming and only 10% engaged in commercial farming. The demographic distribution of farmers is higher in rural areas with 88% of farmers residing in rural settings. Contrary to many other walks of life, more women are engaged in agriculture than men at 56%.

Given the above context, it’s apparent that agriculture is among the major drivers of Rwanda’s economy and will continue to be a national priority. Indeed, the vision 2050 set objective is for the sector to be transformed from labor-intensive, low productivity, and subsistence-based to a mechanised, highly productive agricultural sector with professional farmers and commercialised value chains.

To achieve this, Rwanda has made financing agriculture a priority for achieving a rapid transformation of the agriculture sector and greater financial inclusion.

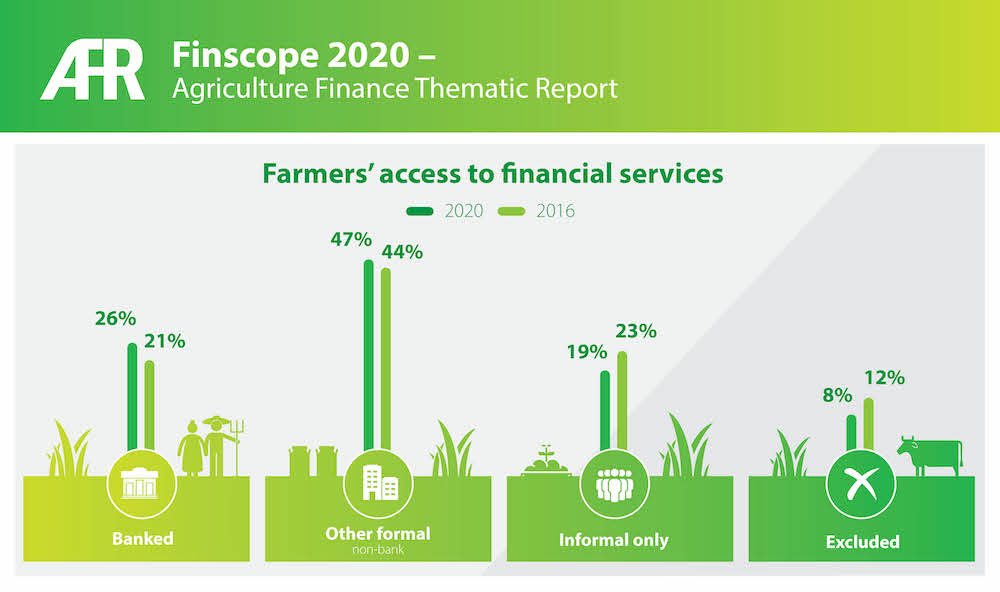

Overall trends in access to finance by farmers

The level of access to financial services and products by farmers is still relatively low despite the increase recorded between 2016 and 2020 as reflected in the Finscope 2020 Agriculture Finance Thematic Report. The report shows an increase in Rwandan banked farmers from 21% in 2016 to 26% in 2020, while the proportion of farmers using other types of formal financial services slightly increased from 44% to 47% over the same period. The usage of informal financial products has decreased from 23% to 19% and this suggests that policy efforts focused on promoting financial inclusion are yielding results, though farmers remain underserved compared to the rest of the population.

The gender gap narrowing progressively

Male farmers have better access to formal financial services, with 77% of them using banks or formal non-bank services, which is 7 percentage points higher than women farmers who are more likely to use informal financial services. Notably, women have become increasingly financially included and the gender gap in using formal financial services (banks and other formal non-bank) has narrowed from 12% in 2016 to 7% in 2020. The proportion of financially excluded women has also decreased more significantly than men, almost bridging the gap in terms of exclusion.

Levels of savings among Rwandan farmers

In 2020, 13% of farmers saved in banks while 35% saved in other formal financial institutions such as SACCOs or mobile money operators. This is significantly more than in 2016 when only 7% of farmers used any kind of formal financial products for their savings. However, a large proportion of farmers still resort to informal savings, even if the share fell from 55% in 2016 to 35% in 2020. Another noticeable change in saving behavior since 2016 is the number of farmers saving money at home which decreased from 26% in 2016 to 2% in 2020.

It is therefore clear that informal savings mechanisms remain important for farmers in Rwanda, and their uptakes are largely driven by the fact that 61% of farmers use savings groups.

Credits accessibility and usage

The Finscope 2020 Agriculture Finance Thematic Report shows that there has been a substantial increase in usage of all sources of credit among Rwandan farmers between 2016 and 2020. Indeed, 76% of farmers have borrowed money in 2020, while only 42% did in 2016. Specifically, the proportion of farmers borrowing from formal financial institutions has doubled from 8% in 2016 to 17% in 2020 including 4% of farmers borrowing money from banks and 12% from other formal institutions (non-bank). However, the main driver of this growth is informal credit, which represented 54% in 2020. It is also interesting to note that only 6% of farmers rely only on their family and friends to borrow money, down from 23% in 2016.

Risk mitigation mechanisms

In 2020, 11% of farmers reported having used formal insurance schemes, which is a significant improvement from the situation in 2016, when only 4% of farmers used insurance schemes. The introduction of the National Agriculture Insurance Scheme (NAIS) in 2019 by the Ministry of Agriculture and Animal Resources (MINAGRI) in partnership with Access to Finance Rwanda greatly contributed to this improvement. However, most farmers remain excluded from insurance services. Underserved farmers when it comes to risk financing, remain close to 90% in both years despite almost threefold increases in insurance penetration from 4% in 2016 to 11% in 2020.

Challenges standing in the way

As Finscope 2020 indicates, there has been a significant increase in access to and usage of financial services among farmers between 2016 and 2020. Nevertheless, some barriers still stand in the way of financial inclusion for farmers ranging from infrastructure bottlenecks, where over 60% of farmers live more than an hour away from financial services access points, inadequate access to products and services of financial services providers (FSPs) and high-risk exposure among farmers. However, there are hopes that the National Agriculture Insurance Scheme (NAIS) will narrow the insurance uptake gaps. Other critical challenges include high loan rejection rates among farmers and the low awareness and usage of Digital Financial Services (DFS) among farmers.

Ways to address existing gaps

The above-mentioned challenges facing farmers while financing their activities need strategic solutions to ensure the envisioned ambitions to transform the agriculture sector into a high-value commercial venture are achieved. The Finscope 2020 Agriculture Finance Thematic Report suggests the following policy recommendations.

Resolve infrastructural bottlenecks that constrain access and usage of financial services among farmers – This requires innovation around infrastructural constraints in serving farmers, and an increased focus on agency banking and digital financial services (DFS) will bring financial services closer to farming communities in Rwanda.

Encourage productive borrowing among farmers – While the uptake of credit products is relatively high among farmers, there is a need for tailored products that enhance borrowing for farming purposes among farmers. Purpose-driven financial products such as input credit schemes, warehouse receipts can encourage productive borrowing among farmers.

Prioritize the provision of risk financing products among farmers – The risk exposure among farmers in Rwanda remains close to 90% between 2016 and 2020 which signifies a big gap in risk financing in Rwanda. FSPs such as insurers, banks, and Mobile Network Operators (MNOs) see this as a market opportunity that they can tap into using agricultural insurance-related products.

Leverage informal savings groups to increase agricultural insurance uptake – Savings groups could be leveraged to increase the uptake of agricultural insurance products e.g., the National Agriculture Insurance Scheme (NAIS) by supporting these groups to save up regularly for insurance premiums, raise awareness on the benefits of agricultural insurance and facilitate the enrolment into the NAIS with the support of the Ministry of Agriculture and Animal Resources (MINAGRI).

Establish de-risking mechanisms to enhance FSPs participation in agricultural lending. Income is one of the big constraining factors to agricultural finance in Rwanda. This demonstrates the need for financial services providers to waive some of the lending requirements (such as collateral) that restrict access to financing among farmers. Government can also consider setting up a guarantee scheme that can cushion FSPs from the heightened lending risks as some of the requirements are relaxed by FSPs.

Read and Download the Finscope 2020 Agriculture Finance Thematic Report